- Matt Bodnar

- Posts

- Uncovering Valuations: Is This Deal Overvalued?

Uncovering Valuations: Is This Deal Overvalued?

Matt Bodnar

September 26, 2024

One of the best ways to build your deal skillset is to fire up a listing and get to work evaluating an existing deal on the market. Today, we dive deep into an e-commerce deal that caught my eye over the weekend. This case study demonstrates how to rapidly evaluate an opportunity, get a quick snapshot of the pros and cons, and determine if a company is overvalued—all within about five minutes.

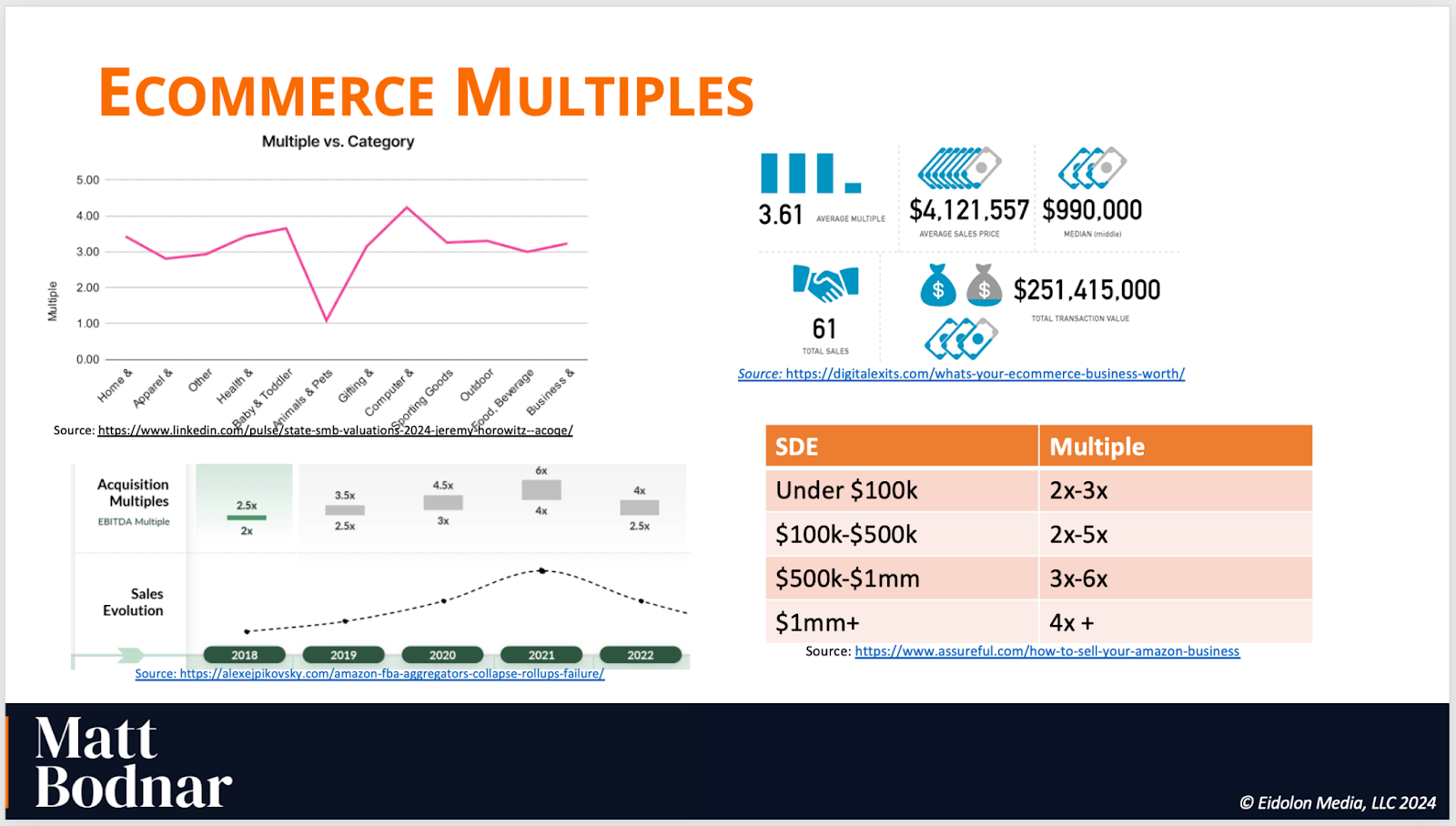

Understanding Market Multiples

Market multiples provide a benchmark for evaluating a company’s value. They anchor the conversation around whether a valuation is reasonable. In e-commerce, multiples typically range from 2x to 4x, depending on various factors such as size, sector, and growth potential.

For instance, a simple Google search on "e-commerce multiples" showcases the following multiples:

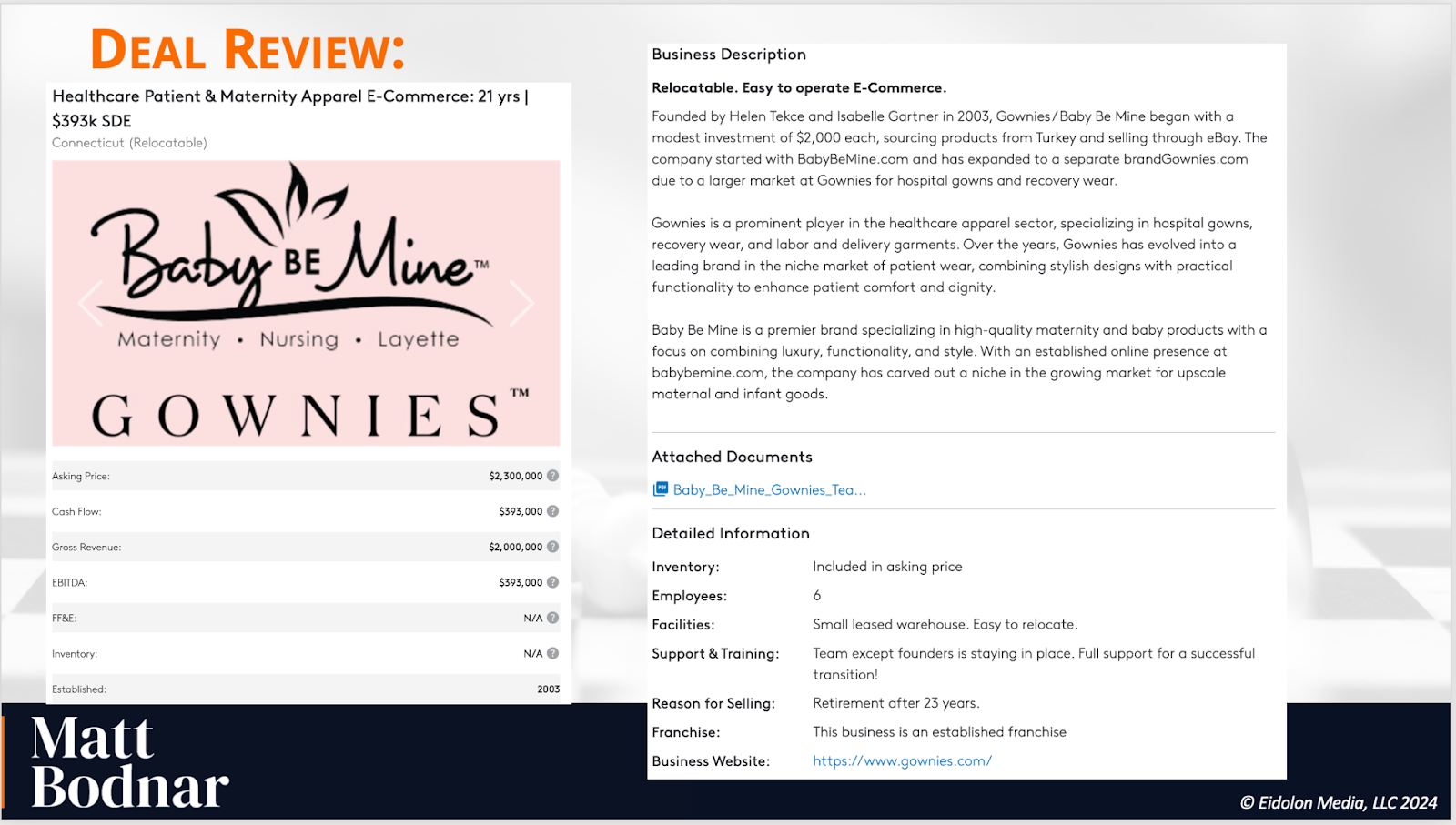

Case Study: Gownies

Let's put this knowledge to use by evaluating Gownies, an e-commerce business listed for $2.3 million on BizBuySell.

Initial Data:

Asking Price: $2.3 million

Cash Flow: $393,000

Gross Revenue: $2 million

EBITDA: $393,000

Sector: Healthcare apparel, specializing in hospital gowns and labor and delivery garments.

Employees: 6

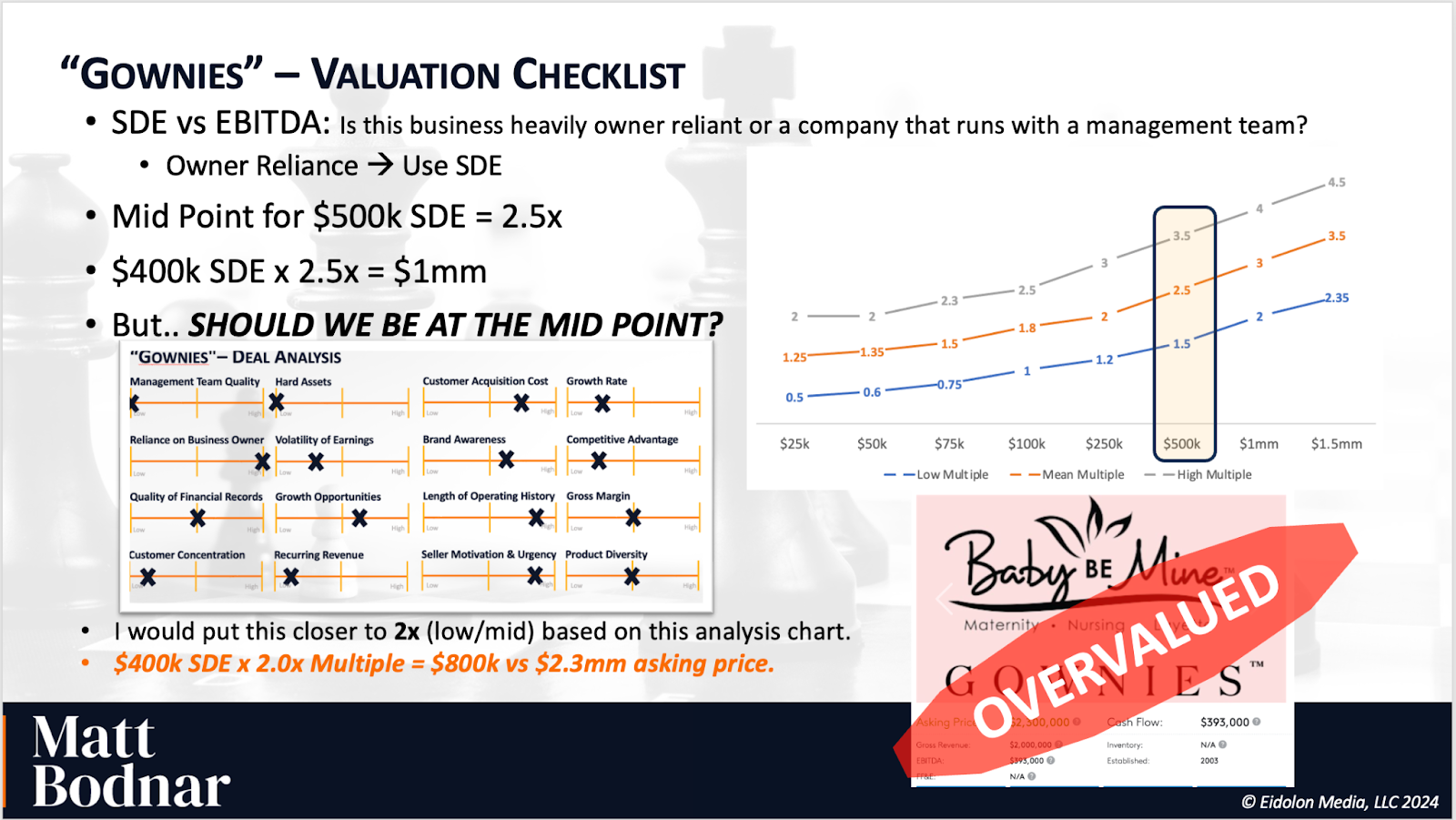

Evaluating Gownies

Based on the limited publicly available information, here’s my initial assessment of several key company specific factors:

Management Team Quality: Low, as both founders are leaving.

Reliance on Business Owner: Likely High.

Quality of Financial Records: Midpoint.

Customer Concentration: Low.

Hard Assets: Little to none.

Volatility of Earnings: Assumed low.

Growth Opportunities: Moderate.

Recurring Revenue: Low.

Customer Acquisition Costs: Moderately high.

Brand Awareness: Slightly above medium.

Length of Operating History: Over 20 years.

Seller Motivation and Urgency: Medium.

Growth Rate: Low.

Competitive Advantage: Uncertain.

Gross Margin: Midpoint.

Product Diversity: Moderate.

Valuation Analysis:

Given the data, should we use Seller's Discretionary Earnings (SDE) or EBITDA? Considering the business is heavily owner-reliant and lacks a substantial management team, SDE feels like the appropriate metric.

Based on market multiples:

Midpoint Multiple: 2.5x

SDE: $400,000

Midpoint Valuation: $1 million

However, given the high owner reliance and other factors, a 2x multiple might be more reasonable, leading to an $800,000 valuation.

Conclusion: Substantially Overvalued

Gownies is asking for $2.3 million, which translates to nearly a 6x multiple on its $400,000 SDE. This is far above the market norm. Even at the higher end of the spectrum (4x multiple), the valuation would be $1.6 million—still significantly less than the asking price.

Therefore, Gownies appears to be substantially overvalued. It’s unlikely to transact at its current price, given the market conditions and benchmarks.

Key Takeaways

Market multiples are invaluable for quick evaluations.

Valuation ranges for e-commerce businesses typically fall between 2x and 4x.

Understanding key metrics helps determine the appropriate multiple for a specific business.

Gownies at $2.3 million is significantly overvalued based on its cash flow and industry norms.

By honing your mastery these principles, you can make informed decisions and avoid overpaying for acquisitions. If you have any questions or need further insights, just hit reply and let me know what you're thinking.

Thank you for being a subscriber to the Deal Mastery Insider!

-Matt

P.S. Not getting enough deals?

Let’s fix that. The Business Acquisition Accelerator is here to help! Get more deals, drive growth, and achieve success with strategies that are proven to work along with a team of expert deal-makers.

Say goodbye to deal flow challenges and embrace a future full of opportunities for your business.

See ya inside.